- Courses

- GS Full Course 1 Year

- GS Full Course 2 Year

- GS Full Course 3 Year

- GS Full Course Till Selection

- Answer Alpha: Mains 2025 Mentorship

- MEP (Mains Enrichment Programme) Data, Facts

- Essay Target – 150+ Marks

- Online Program

- GS Recorded Course

- Polity

- Geography

- Economy

- Ancient, Medieval and Art & Culture AMAC

- Modern India, Post Independence & World History

- Environment

- Governance

- Science & Technology

- International Relations and Internal Security

- Disaster Management

- Ethics

- NCERT Current Affairs

- Indian Society and Social Issue

- NCERT- Science and Technology

- NCERT - Geography

- NCERT - Ancient History

- NCERT- World History

- NCERT Modern History

- CSAT

- 5 LAYERED ARJUNA Mentorship

- Public Administration Optional

- ABOUT US

- OUR TOPPERS

- TEST SERIES

- FREE STUDY MATERIAL

- VIDEOS

- CONTACT US

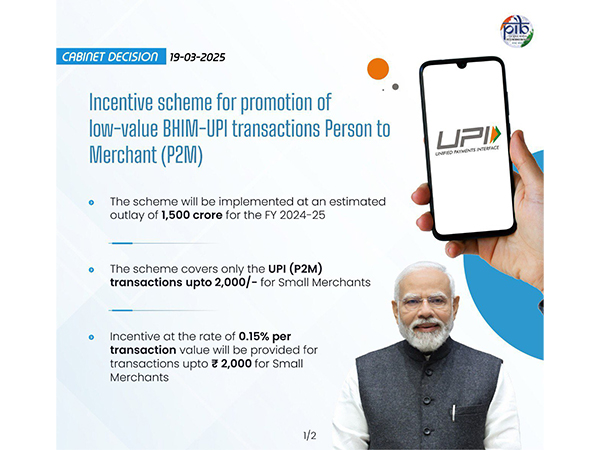

Cabinet Approves Incentive Scheme for Promotion of Low-Value BHIM-UPI Transactions (P2M)

Cabinet Approves Incentive Scheme for Promotion of Low-Value BHIM-UPI Transactions (P2M)

- The Union Cabinet, led by Prime Minister Shri Narendra Modi, has approved an Incentive Scheme for promoting low-value BHIM-UPI transactions (P2M) for the financial year 2024-25.

- The scheme will be implemented with an estimated budget of ₹1,500 crore, running from 1st April 2024 to 31st March 2025.

Background:

- Digital Payment Strategy: The government aims to increase financial inclusion and provide a variety of payment options to promote digital transactions.

- Merchant Discount Rate: MDR is the fee that a merchant (business owner) has to pay to the bank or payment service provider when a customer makes a payment using a debit card, credit card, or digital payment methods like UPI. It is essentially a percentage of the transaction amount.

- Traditionally, MDR was applicable (up to 0.90% for debit cards and 0.30% for UPI P2M).

- However, since January 2020, MDR has been made zero for RuPay Debit Cards and BHIM-UPI transactions to encourage digital payments.

Incentive Scheme Overview:

The Incentive Scheme is designed to support RuPay Debit Cards and low-value BHIM-UPI transactions (P2M).

- Yearly Incentive Payout (₹ in Crores):

- FY 2021-22: ₹1,389 crore (Total), ₹957 crore for BHIM-UPI

- FY 2022-23: ₹2,210 crore (Total), ₹1,802 crore for BHIM-UPI

- FY 2023-24: ₹3,631 crore (Total), ₹3,268 crore for BHIM-UPI

- Incentive Distribution: Paid to acquiring banks (merchant's bank) and shared with other stakeholders, including issuer banks, payment service provider banks, and app providers.

Key Features:

Eligibility:

- Small Merchants: UPI transactions up to ₹2,000 will be covered under the scheme.

- Large Merchants: No incentive for transactions above ₹2,000.

Incentive Structure:

- Small Merchants: An incentive of 0.15% per transaction for transactions up to ₹2,000.

- Large Merchants: No incentives for any transaction value.

How it Works: Incentive Distribution:

- 80% of the admitted claim amount will be disbursed to acquiring banks each quarter without any conditions for quick reimbursement.

- The remaining 20% will be disbursed if the bank meets the following performance conditions:

- 10% Bonus: If the bank's technical decline rate is below 0.75%.

- 10% Bonus: If the bank maintains a system uptime of over 99.5%.

Benefits:

For Customers:

- Seamless & Charge-Free Payments: Customers can continue using UPI for everyday purchases (e.g., groceries, tea, etc.) without extra charges.

- It is to ensure that there is no added financial burden on consumers making small purchases via UPI.

For Small Merchants:

- Incentive at 0.15% per Transaction: Small merchants can accept UPI payments without worrying about transaction fees.

- This encourages more small businesses to adopt digital payments and makes it easier for them to embrace UPI as a payment method.

For the UPI Ecosystem:

- Zero MDR: No Merchant Discount Rate (MDR) is charged on UPI transactions.

- This is making it cost-effective for merchants to accept digital payments.

No Benefits for Large Merchants:

- The incentive applies only to small merchants, ensuring support for local businesses rather than large-scale businesses.

Growth in Digital Payments:

- The total digital payment transactions have increased significantly from ₹8,839 crore in FY 2021-22 to ₹18,737 crore in FY 2023-24, with a CAGR of 46%.

- The number of UPI transactions has grown from ₹4,597 crore in FY 2021-22 to ₹13,116 crore in FY 2023-24.

Objectives:

- Promote BHIM-UPI: To achieve a transaction volume of ₹20,000 crore in FY 2024-25.

- Infrastructure Strengthening: Support participants in building a secure and robust digital payment system.

- Enhance UPI Reach: Increase penetration of UPI in tier 3-6 cities, especially rural and remote areas using solutions like UPI 123PAY and UPI Lite/UPI LiteX.

- Quality Assurance: Maintain high system uptime and minimize technical declines.

An introduction to NPCI and its various products

- National Payments Corporation of India (NPCI) is an initiative of the Reserve Bank of India (RBI) and the Indian Banks’ Association (IBA) established under the Payment and Settlement Systems Act, 2007.

- NPCI aims to transform India into a ‘less-cash’ society by providing accessible payment services to every Indian, thereby advancing its vision to become the best payments network globally.

Legal Status:

- NPCI is registered as a “Not for Profit” Company under the provisions of Section 8 of the Companies Act 2013.

- Its objective is to provide infrastructure for both physical and electronic payment and settlement systems in India.

NPCI Products :

- RuPay

- RuPay is an indigenous payment system designed to meet Indian consumer, bank, and merchant needs.

- It supports debit, credit, and prepaid cards issued by banks in India, promoting retail electronic payments.

- Collaborates with international network partners for global acceptance and world-class payment solutions.

- IMPS (Immediate Payment Service) : India leads the world in real-time payments in the retail sector with IMPS.

- NACH (National Automated Clearing House) : Provides an electronic mandate platform for bulk push and pull transactions, facilitating paperless collection processes for corporates and banks.

- APBS (Aadhaar Payment Bridge System) : Facilitates Direct Benefit Transfers for various Central and State-sponsored schemes, aiding government agencies.

- AePS (Aadhaar enabled Payment System) : Drives financial inclusion by providing doorstep access to funds, particularly in underserved areas.

- NFS (National Financial Switch) : Largest network of shared ATMs in India, enabling interoperable cash withdrawal, funds transfer, and other value-added services.

- UPI (Unified Payments Interface) : It makes it easy to send and receive by just scanning a QR code or using a user’s phone number. Unlike most digital payment systems, the amount gets directly debited to the linked bank account.

- Bharat Bill Payment System : Offers a one-stop bill payment solution for recurring payments across various categories, enhancing consumer convenience.

- NETC (National Electronic Toll Collection) : Meets electronic tolling requirements in India through FASTag, enabling electronic toll payments without stopping at toll plazas..

List of countries that accept UPI :

|

Sr.no |

Country Name |

|

1 |

Bhutan (first countries to adopt UPI payments outside India) |

|

2 |

France (E-commerce) (first countries in the European region to access UPI payments) |

|

3 |

Mauritius launched UPI payments on February 12, 2024. |

|

4 |

Singapore |

|

5 |

Sri Lanka |

|

6 |

UAE embraced UPI in August 2021. ( 3rd-largest trade partner of India) |

|

7 |

Nepal |

List of countries that accept RuPay :

|

Sr.no |

Country Name |

|

1 |

South Asia: Bhutan, Nepal, Sri Lanka, Maldives (Bhutan is first countries to adopt and issue RuPay bank cards) |

|

2 |

Southeast Asia: Singapore |

|

3 |

Middle East: UAE, Oman |

|

4 |

Europe: France |

|

5 |

Other: Mauritius |

|

Also Read |

|

| NCERT Books For UPSC | |

| UPSC Monthly Magazine | Best IAS Coaching in Delhi |

India’s Rising 'Invisible' Exports

India’s State Capacity and Qing Dynasty Lessons

EU’s 2040 Climate Plan and Carbon Credits

Karol Bagh Metro Pillar No. 112, Above Domino's, 22B, First Floor, New Delhi - 110060

Very Important Instruction For Any Issue, Student Must Produce His/Her Fee Receipt. Without Fee Receipt, It Will Not Be Possible To Track Your Details. If You Have Been Given Any Special Consideration, You Must Keep That In Writing And Produce In Case Of Conflict.

Copyright © 2024-2026 ENSURE IAS. All rights reserved.