The Cash Reserve Ratio (CRR) and the Statutory Liquidity Ratio (SLR) are the primary pillars of the Reserve Bank of India’s (RBI) monetary policy. These tools are strategically utilized to regulate the money supply, manage inflation, and ensure the inherent stability of the Indian banking system. By adjusting these ratios, the RBI directly influences the lending capacity of banks and the overall liquidity available in the economy.

Understanding the Cash Reserve Ratio (CRR)

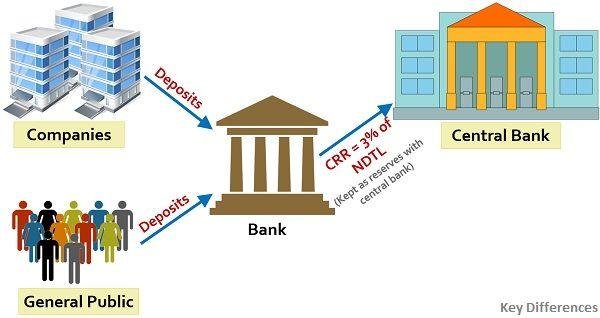

The Cash Reserve Ratio (CRR) refers to the specific share of a bank’s total deposits that must be maintained with the Reserve Bank of India (RBI) exclusively in the form of cash.

1. Key Characteristics of CRR

- Maintenance with RBI: Banks are mandated to keep this reserve with the central bank (RBI) rather than holding it themselves.

- Zero Interest: The RBI does not provide any interest payments on the funds maintained as CRR.

- Usage Restrictions: Banks are strictly prohibited from using CRR funds for lending or investment

- Applicability: All scheduled commercial banks (including foreign banks operating in India), regional rural banks, and specific co-operative banks are mandated to comply with CRR requirements.

- Non-Banking Financial Companies (NBFCs) are excluded from the purview of CRR requirements.

2. Legal Framework of CRR

- RBI Act 1934: Section 42 of the Act provides the legal basis for the RBI to mandate a CRR.

- Ceiling Limits: Originally, the Act provided for a range between 3% and 15%.

- 2007 Amendment: An amendment in 2007 removed the lower floor of 3%, allowing the RBI flexibility to set the CRR anywhere between 0% and 15%.

Core Objectives of the Cash Reserve Ratio

The RBI utilizes CRR to achieve several critical macroeconomic and systemic goals:

- Ensure Safety of Depositor Money: By keeping a portion of deposits with the RBI, it ensures banks do not exhaust their cash reserves during financial emergencies.

- Control Money Supply: It allows the RBI to instantly increase or decrease the volume of money banks have available to lend.

- Manage Inflation: Increasing the CRR helps suck out excess liquidity from the system, which is essential for controlling rising prices.

- Maintain Financial Stability: It serves as a vital buffer that preserves the health of individual banks and the wider financial system.

- Improve Liquidity Discipline: It mandates that banks maintain a minimum level of ready cash, preventing them from over-extending through excessive lending.

- Support Monetary Policy: CRR is a fundamental instrument for the RBI to regulate the overall flow of credit within the Indian economy.

The Incremental Cash Reserve Ratio (I-CRR)

The Incremental Cash Reserve Ratio (I-CRR) is a specialized, temporary measure used by the RBI to address sudden surges in liquidity.

- Definition: Unlike standard CRR, which applies to total deposits, I-CRR is imposed only on incremental (new) deposits over a specific timeframe.

- Purpose: Its primary function is to absorb a sudden surplus of liquidity that could lead to macroeconomic disruptions.

- Case Study (August 2023): On 10 August 2023, the RBI mandated a 10% I-CRR on the increase in Net Demand and Time Liabilities (NDTL) recorded between 19 May 2023 and 28 July 2023.

- Trigger Factor: This 2023 mandate was triggered by the massive return of ₹2,000 currency notes to the banking system, which created a liquidity surplus.

Statutory Liquidity Ratio (SLR): The Self-Maintained Reserve

While CRR is kept with the RBI, the Statutory Liquidity Ratio (SLR) is the percentage of deposits that banks must maintain with themselves.

- Forms of Assets: SLR can be held in the form of liquid cash, gold deposits, or government-approved securities.

- Objective: It is primarily used to control inflation and ensure that banks maintain a portion of their assets in safe, liquid forms.

- Inflation Control: Increasing the SLR reduces the money supply available for lending, thereby helping to cool down an overheating economy.

Economic Impact of Adjusting the Cash Reserve Ratio

Changes in the CRR have a direct “multiplier effect” on the Indian economy.

1. Impact of Increasing CRR

- Reduced Liquidity: Banks have fewer funds available for day-to-day operations as more cash is locked with the RBI.

- Lower Lending Capacity: The ability of banks to provide loans to households and businesses is curtailed, slowing credit growth.

- Rising Interest Rates: Tighter liquidity often leads to an increase in interest rates.

- Inflation Suppression: By reducing the money supply, it effectively helps in lowering inflation.

2. Impact of Decreasing CRR

- Enhanced Liquidity: Banks gain immediate access to more cash reserves.

- Boosted Lending: Credit growth is supported, encouraging both private investment and consumer spending.

- Easing Interest Rates: Improved liquidity conditions typically lead to a reduction in interest rates.

- Economic Stimulus: It serves to boost economic activity and support growth during periods of slowdown.

Comparative Analysis: CRR vs. SLR

| Feature | Cash Reserve Ratio (CRR) | Statutory Liquidity Ratio (SLR) |

| Maintained With | The Reserve Bank of India (RBI) | The Banks themselves |

| Form of Reserve | Cash only | Cash, Gold, or Government Securities |

| Interest Earned | No interest is paid by the RBI | Banks earn interest/returns on securities/gold |

| Purpose | Controls money supply and ensures bank solvency | Limits credit expansion and ensures investment in the government bonds |

Frequently Asked Questions (FAQs)

What is the current range for CRR as per the RBI Act?

The RBI can set the CRR anywhere between 0% and 15% following the 2007 amendment to the RBI Act 1934.

Does the RBI pay interest on the money kept as CRR?

No, the RBI does not provide any interest on the funds maintained under the Cash Reserve Ratio.

Can banks use CRR funds to buy government bonds?

No, CRR must be kept in the form of cash only and cannot be used for any lending or investment purposes.

In what forms can a bank maintain its SLR?

Banks can maintain their Statutory Liquidity Ratio in the form of liquid cash, gold, or government securities.

Which financial institutions are exempt from maintaining CRR?

While commercial and regional rural banks must maintain CRR, Non-Banking Financial Companies (NBFCs) are excluded.

What happens to bank lending capacity when the RBI increases the CRR?

The lending capacity of banks decreases because a larger portion of their deposits is locked with the RBI and cannot be used for loans.

What was the reason for introducing Incremental CRR in August 2023?

It was introduced to absorb the surplus liquidity generated by the return of ₹2,000 currency notes to the banking system.

How does SLR help in controlling inflation?

Increasing the SLR forces banks to keep more deposits in liquid assets or securities, which reduces the money supply available for lending to the public.

What is the fundamental difference in where CRR and SLR are kept?

CRR is maintained with the RBI, whereas SLR is maintained by the banks themselves within their own vaults or accounts.

Is I-CRR calculated on the total deposits of a bank?

No, I-CRR is a temporary requirement imposed only on the incremental (new) deposits received during a specific period, not the total deposits.

Would you like me to explain the current rates for CRR and SLR as of the latest RBI bi-monthly monetary policy review?